Beyond Nvidia: Why Billionaires Are Quietly Cornering the Quantum Market with Alphabet

Billionaires are dumping Nvidia for Alphabet. Discover why smart money is betting $126B on Google’s "Willow" quantum chip and cloud dominance.

By – Sevs Armando

Key Takeaways

Smart Money Rotation: Top fund managers, including Seth Klarman and Bill Ackman, are reducing Nvidia exposure to accumulate Alphabet (GOOGL), citing valuation concerns.

The Quantum Moat: Google’s "Willow" QPU recently outperformed supercomputers by 13,000x, signaling a tangible lead in the commercialization of quantum mechanics.

Cash is King: With $126.8 billion in liquidity and $165 billion in operating cash flow, Alphabet possesses the capital structure to outspend rivals in the capital-intensive AI/Quantum race.

Valuation Arbitrage: While Nvidia trades at bubble-territory multiples (P/S > 30), Alphabet’s growth-adjusted valuation offers a defensive hedge against a potential tech correction.

The retail crowd is still chasing Nvidia, but the "Smart Money" has already left the building.

While the wider market fixates on GPU scarcity and Nvidia’s latest Blackwell chips, a notable divergence has emerged in 13F filings. Billionaire investors—including Seth Klarman, Chase Coleman, and Bill Ackman—are rotating capital out of the high-flying hardware giant and into a legacy tech player that the market has arguably taken for granted: Alphabet (GOOGL).

This isn't just a value play; it is a bet on the next decade of compute infrastructure. The narrative that Nvidia owns the future of AI is being challenged by a simpler, more brutal financial reality: hardware creates the infrastructure, but platforms capture the recurring revenue.

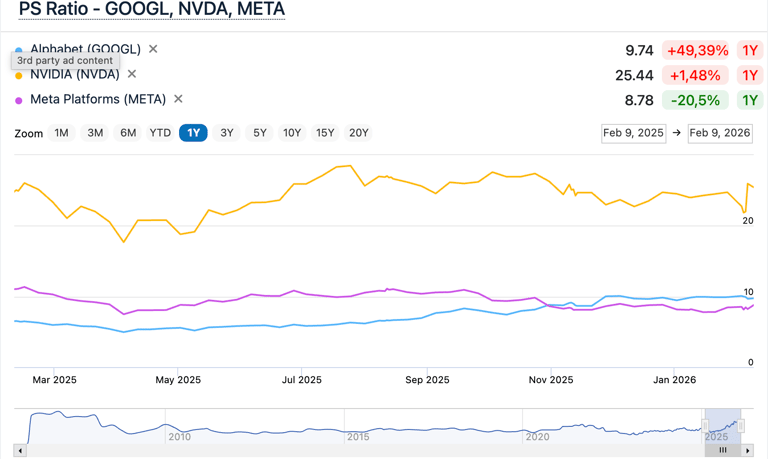

The "Money Impact": Valuation Disconnect

The current market structure presents a classic arbitrage opportunity for institutional investors. Nvidia has been priced for perfection, trading at a Price-to-Sales (P/S) ratio exceeding 30—a historical marker for asset bubbles. In contrast, Alphabet trades at a discount relative to its long-term free cash flow potential, despite posting a 47% surge in Google Cloud revenue in Q4 2025.

Investors are essentially paying a premium for Nvidia's past performance while getting Alphabet's future optionality—specifically in quantum computing—at a discount.

Strategic Implications: The Quantum Leap (Willow vs. Silicon)

The real story here is not Search; it is the transition from binary to quantum compute.

In December 2024, Alphabet debuted its "Willow" Quantum Processing Unit (QPU). Unlike theoretical setups, Willow is operational. In October 2025, it executed a quantum algorithm 13,000 times faster than the world’s fastest supercomputers.

Winners & Losers in the Quantum Era (2026-2035)

The Disrupted (Losers): Traditional encryption firms and legacy logistic optimization software. Quantum computing renders current RSA encryption obsolete and solves optimization problems (like global shipping routes or protein folding) in seconds rather than centuries.

The Aggregators (Winners): Alphabet and Microsoft. By integrating QPUs like Willow into their cloud infrastructure (Google Cloud), these giants will rent quantum power to pharmaceutical and logistics companies. They become the "utility providers" of the quantum age.

This creates a flywheel effect: Google Cloud attracts high-value enterprise clients who need quantum capabilities, further funding the R&D required to maintain quantum supremacy.

What is a QPU?

QPU (Quantum Processing Unit) is the brain of a quantum computer. Unlike a CPU or GPU which processes bits (0s and 1s), a QPU uses qubits. Qubits can exist in a state of superposition (representing both 0 and 1 simultaneously), allowing them to perform massive, parallel calculations that are impossible for classical silicon chips.

The Defensive Growth Play

The rotation into Alphabet suggests that high-net-worth portfolios are shifting to "Defensive Growth." They want exposure to AI and Quantum upside but are unwilling to stomach the volatility and valuation risk associated with pure-play hardware stocks like Nvidia.

Alphabet offers a fortress balance sheet—$126.8 billion in cash reserves—acting as a buffer against macro headwinds. For the investor looking 5 to 10 years out, the question is not who sells the chips today, but who owns the cloud where the quantum future lives.

Provocative Question: If quantum computing breaks current encryption standards by 2030, does owning the company that controls the "switch" (Alphabet) become a matter of national security rather than just portfolio allocation?

FAQ

1. Why are billionaires selling Nvidia for Alphabet? Institutional investors often rotate capital to manage risk. Nvidia's valuation (P/S > 30) implies it must execute perfectly for years to justify its price. Alphabet offers similar exposure to AI and Cloud trends but at a much lower valuation multiple, providing a "margin of safety."

2. How does the "Willow" chip impact Google's stock price? Currently, the market views quantum computing as a "science project," barely pricing it in. However, as "Willow" integrates into Google Cloud to solve commercial problems (drug discovery, materials science), it unlocks a new, high-margin revenue stream that could drive multiple expansion.

3. Is Google Search still a monopoly risk? Yes. While Google holds ~90% of the search market, antitrust regulation remains a threat. However, the bull case argues that Google's diversification into Cloud and Quantum computing reduces its reliance on ad revenue, making a potential breakup less devastating than previously thought.

Related Stories

The Money Impact © 2026

Business and finance explained by impact.