Consumer Liquidity: Why Top Investors Treat Credit Cards as 0% Leverage, Not Debt

Stop treating credit cards like debt traps. Discover how top investors use the "Float" and rewards to earn 0% leverage while others pay the "poor tax."

By – Sevs Armando

Key Takeaways

The Liquidity Arbitrage: While 48% of Americans pay double-digit interest (APR), sophisticated investors use the 21-55 day "grace period" as an interest-free float to preserve working capital.

The Transactor Premium: Banks classify users as "Transactors" (profitable via data/fees) or "Revolvers" (profitable via interest). Being a Transactor unlocks perks that essentially subsidize your lifestyle at the expense of Revolvers.

Credit as an Asset Class: Your credit score is no longer just a reputation metric; it is an access key to leverage. In a high-rate environment, a 750+ score is the only gateway to sub-prime rates.

The Trap of Minimums: Paying only the minimum due is mathematically designed to turn a $1,000 purchase into a $3,000 liability over a decade.

"Credit is fire. It cooks your food or burns your house down."

That adage is cute, but it’s outdated. In the current financial architecture, credit is not just a tool; it is a weapon of liquidity.

Most consumers view credit cards as a necessary evil or a temptation to overspend. This binary thinking is expensive. For the high-net-worth individual, a credit card is a precision instrument used for Interchange Arbitrage and Cash Flow Float.

According to recent data from The Motley Fool, the divide between those who use the bank and those who are used by the bank has never been wider. If you are paying APR, you are the product. If you are farming rewards and floating cash, you are the partner.

Here is why the "Beginner’s Guide" model of credit is insufficient for building real wealth—and how to flip the script.

The "Money Impact": The Cost of Carry vs. The Float

The entire credit card industry is built on a cross-subsidy model. The "Revolvers" (people who carry a balance) pay for the flights, hotels, and cash back of the "Transactors" (people who pay in full).

The Trap: Variable APRs move with the market. In 2026, carrying a balance means paying 20-29% interest. This destroys wealth faster than any bear market.

The Strategy: The "Float." When you buy something on Day 1 of your billing cycle, you don't actually pay for it until the due date—often 50+ days later. During that time, your cash sits in a High-Yield Savings Account (HYSA) or Money Market Fund earning 4-5%. You are effectively borrowing at 0% to earn 5%.

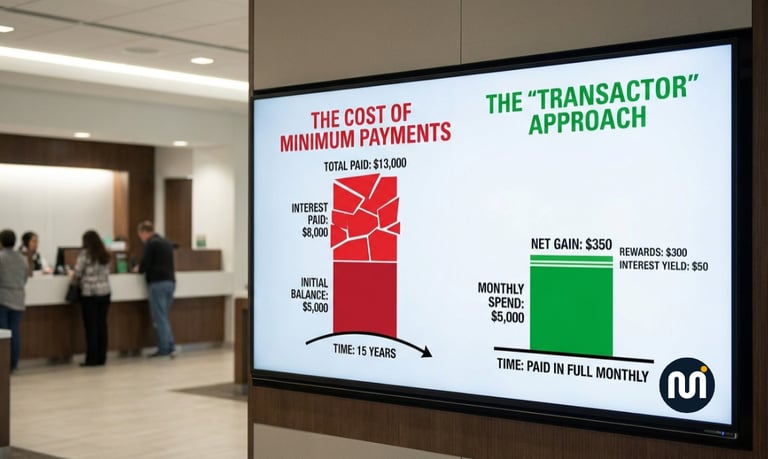

[Visual Placeholder] Insert Chart: "The Cost of Minimum Payments." A graph showing a $5,000 balance paid off at minimums (taking 15 years and costing $8,000 in interest) vs. the "Transactor" gaining $300 in rewards and $50 in interest yield on the same spend.

The Death of Cash (2026-2030)

Winners & Losers

Losers: Cash Loyalists. Using debit or cash is a guaranteed -1% to -3% return on spend due to missed rewards and fraud protection. You are paying the merchant's credit card processing fees (baked into prices) without getting the rebate.

Winners: The Algorithmic Borrower. Consumers who automate their utilization ratios to stay under 10% will dominate.

The Evergreen Angle: As we move toward a fully digital currency environment, "Creditworthiness" will morph into "Reputation Capital." Your ability to manage unsecured debt will determine your access to housing and insurance premiums even more aggressively than it does today.

What is "Interchange Arbitrage"?

Interchange Arbitrage refers to the strategy of using a credit card to pay for expenses to capture the "interchange fee" (swipe fee) kickback in the form of rewards (points/cash back). Merchants pay ~2-3% to accept cards; sophisticated users reclaim this margin, effectively discounting their entire life by 2-3% while the cash sits in their account earning interest until the bill is due.

Stop Playing Defense

The standard advice—"pay your bill on time"—is defensive. It keeps you out of trouble, but it doesn't get you ahead.

To win in 2026, you must play offense. Treat your credit limit as a Line of Credit (LOC) that you never pay interest on. Use the bank's money to facilitate your life while your money works for you. If you are not extracting at least $1,000 a year in value from your issuer, you are leaving money on the table.

If the bank offers you a 30-day interest-free loan every month (the grace period) and you use a debit card instead, are you financially illiterate or just charitable to the bank?

FAQ

1. Does checking my credit score actually hurt it? No. This is a persistent myth. Checking your own score is a Soft Pull and has zero impact. Applying for a new card is a Hard Pull, which causes a temporary (5-10 point) dip. In the long run, the dip is irrelevant compared to the benefits of a higher total credit limit.

2. Why do wealthy people use "Secured Cards"? They usually don't, but they use the concept. Secured cards are collateralized loans. You put down $500 to get a $500 limit. It’s the fastest way to repair a damaged reputation because there is zero risk to the issuer. It’s the "training wheels" of leverage.

3. Is the "0% Intro APR" a trap? It is a loaded gun. If you use it to consolidate debt and pay it off, it is a wealth-building tool. If you use it to delay the pain of overspending, it is a time bomb. If you still have a balance when the promo period ends, you are often hit with retroactive interest or an immediate jump to 29% APR.

Related Stories

The Money Impact © 2026

Business and finance explained by impact.