The "Lag" Is Over: Why the Bill for the 2025 Boom Is Finally Coming Due

LATESTECONOMY

As the 2026 fiscal year begins, the "lag" protecting consumers from tariffs and labor shortages is vanishing. We analyze the structural shift from efficiency to resilience and what it means for business.

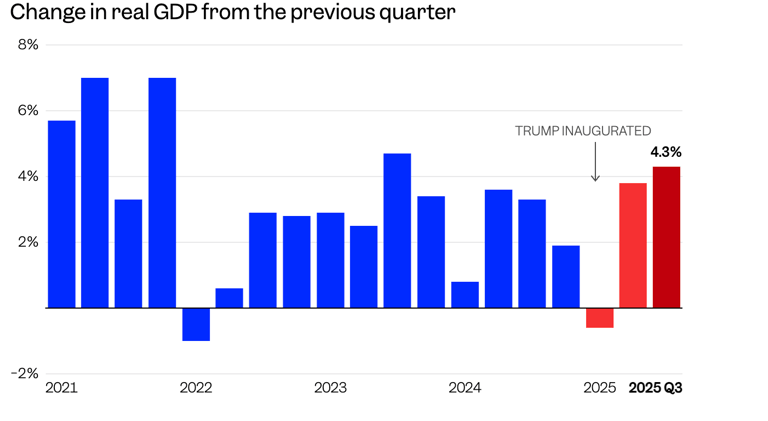

For the past twelve months, the U.S. economy has existed in a state of suspended animation—a "Goldilocks" zone where aggressive protectionist policies were announced, but their economic consequences seemed to miraculously vanish. The data from President Trump’s first year back in the White House painted a confusing, almost paradoxical picture: historic tariffs were levied, yet consumer prices remained relatively stable. Immigration was sharply restricted, yet corporate earnings roared.

As we enter 2026, that buffer has evaporated. The "economic miracle" of the last year was not a victory of new policy, but a withdrawal from old savings. We are now witnessing the death of the "lag"—the time delay between a policy’s implementation and its presence at the cash register. The 2025 economy was financed by borrowing from the future; 2026 is when the bill comes due.

The Great Inventory Illusion

The most dangerous misconception in modern economics is that a tax on trade appears instantly in the price of milk or microchips. It does not. The primary reason inflation remained dormant last year, despite tariffs averaging 10-20% on key imports, was a massive, invisible shield: pre-tariff inventory.

Throughout late 2024 and early 2025, savvy importers and logistics giants stockpiled goods at unprecedented rates. For nearly a full year, the American retail sector was largely powered by "legacy" stock—goods purchased under the old tax regime but sold during the new political era. This created a temporary artificial paradise where the government collected tariff revenue, corporations maintained margins, and consumers saw stable prices.

That era is mathematically over. Supply chain data indicates that these pre-tariff stockpiles are effectively depleted. Retailers are now restocking at the new, higher cost basis. The "pass-through" rate—the percentage of the tariff cost transferred to the consumer—is shifting from a negligible 20% in 2025 to near 100% in 2026. The price stability of the last year wasn’t a structural reality; it was an accounting trick that has run its course.

The "Help Wanted" Inflation Spiral

While the goods sector was shielded by inventory, the services sector is now colliding with a different reality: a supply-side labor shock. The administration's aggressive restriction on legal immigration has created a paradox unique to this economic moment—a slowing job market that still cannot find workers.

In a normal cycle, cooling demand leads to cooling wages. But when the supply of labor is artificially capped by policy—removing millions of eligible workers from the pool—businesses lose the ability to negotiate. In sectors like hospitality, construction, and healthcare, the sudden contraction of the workforce has handed remaining employees unprecedented bargaining power.

This drives a "wage-price spiral" that is distinct from the growth-driven raises of a booming economy. Businesses aren't paying more because workers are producing more; they are paying more simply to keep the lights on. This creates "sticky" inflation. Unlike gas prices, which can fall, wage hikes rarely reverse. This structural shift virtually guarantees that core inflation will remain stubbornly above central bank targets, forcing the Federal Reserve into a corner where cutting rates becomes dangerous.

The Limits of "Drill, Baby, Drill"

The energy sector provides the starkest example of the difference between political slogans and market mechanics. While the administration points to lower gas prices in 2025 as a policy win, analysts note that this was largely driven by a global supply glut and record U.S. output that began before the political transition.

Now, the "law of diminishing returns" is setting in. Deregulation has made drilling easier, but it hasn't made it profitable at current price levels. With oil prices hovering near break-even points for many shale producers, capital expenditure is slowing down. We are learning that you can deregulate the permission to drill, but you cannot legislate the profitability of doing so. If global demand ticks up even slightly in 2026, the lack of new investment in 2025 could trigger a price spike that no amount of domestic policy can suppress.

The Market's Dangerous Optimism

Perhaps the most confusing signal for investors has been the divergence between equity markets and credit markets. Stock exchanges have rallied on the "sugar high" of fiscal stimulus and the optical illusion of cost-cutting. Yet, the bond market—often the smarter, if gloomier, sibling—is telling a terrifying story.

Yields are spiking not because growth is accelerating, but because lenders are demanding a higher premium to hold debt in an inflation-prone environment. The bond market is signaling that the era of "easy money" is being replaced by an era of "expensive reality." The disconnect suggests that equity investors are still trading on the 2025 narrative of "resilience," while bond traders are pricing in the 2026 reality of stagflation.

The Future of the "Protected" Economy

If this structural pattern continues, it signals a profound shift in the DNA of the Western economy. We are moving from an era of efficiency—defined by just-in-time supply chains and fluid labor markets—to an era of resilience, which is inherently more expensive.

The long-term future of this industry will likely be defined by a "Nationalism Premium." Companies will no longer compete solely on price or quality, but on their ability to navigate trade barriers and secure scarce labor. For the average consumer and investor, the lesson is stark: Protectionism does not eliminate costs; it merely delays them. The "lag" allowed us to enjoy the party for a year, but the bill has finally arrived.

Related Stories

The Money Impact © 2026

Business and finance explained by impact.